Market Update

1Q2025

May 9, 2025

·

Team

We recently shared this market update as part of our 1Q2025 update to our own investors. We’d like to share this context more broadly as it may be helpful to founders, LPs, VCs, and others elsewhere.

What transpired this quarter came as a surprise to many. After the US election, the expectation was for 2025 to be an unabated bull market but a wave of economic uncertainty shifted the outlook. Rising prices associated with a succession of tariffs imposed by the US administration on other countries raised concerns about renewed inflation in the US economy, which were reflected in the liquid markets: Bitcoin’s market cap fell 12% over the quarter, while Ethereum declined by 46%.

However, as so often happens in crypto, public market price action diverged from the underlying health of the industry.

In stark contrast to the previous administration, the new administration has shown a clear willingness to work with the industry to establish clear regulations and guidelines that support growth. Two key proposed bills, the GENIUS Act and the Digital Asset Market Structure Bill, have advanced through the legislative process and aim to deliver a comprehensive framework for stablecoins and clarify regulatory oversight of digital assets, respectively.

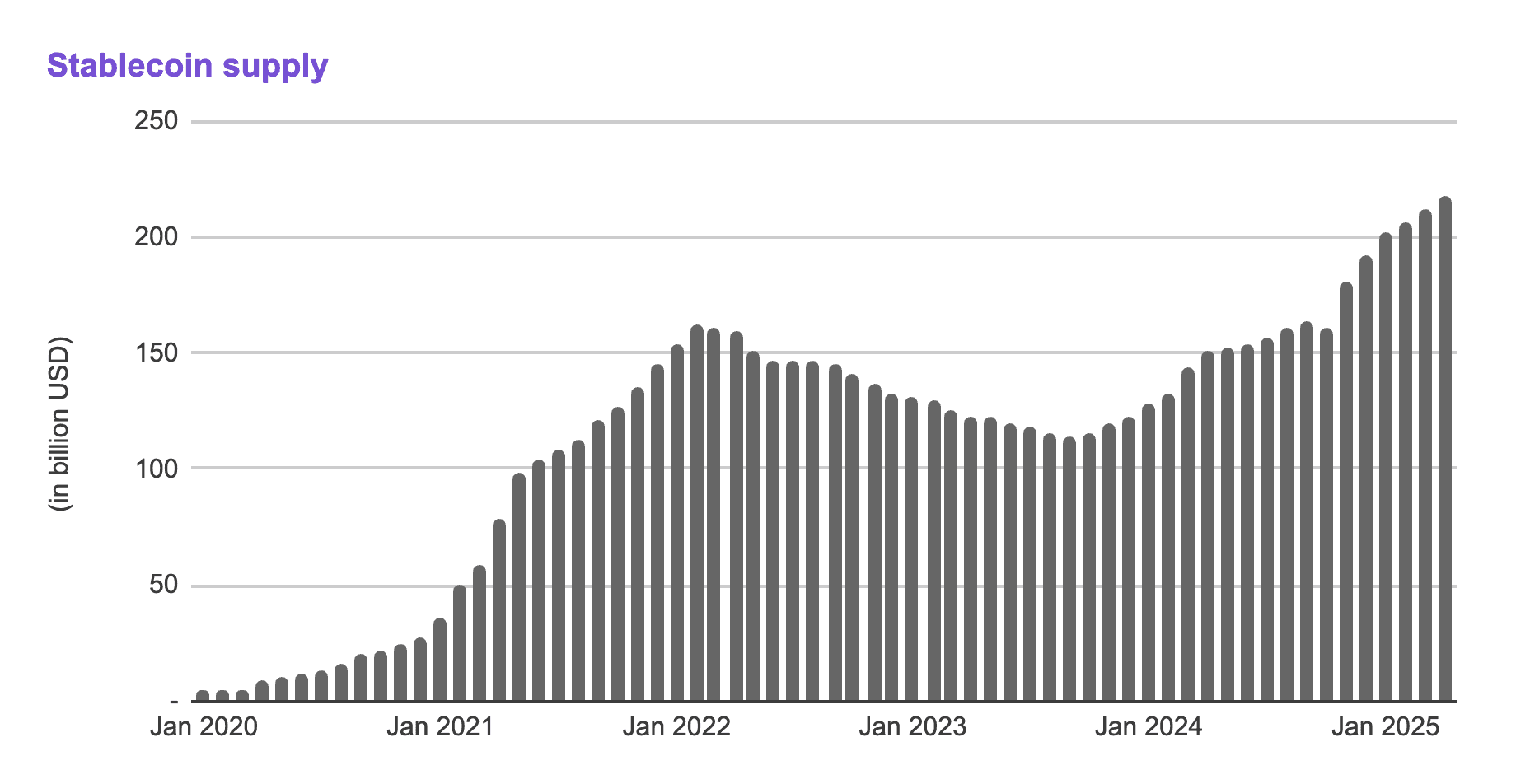

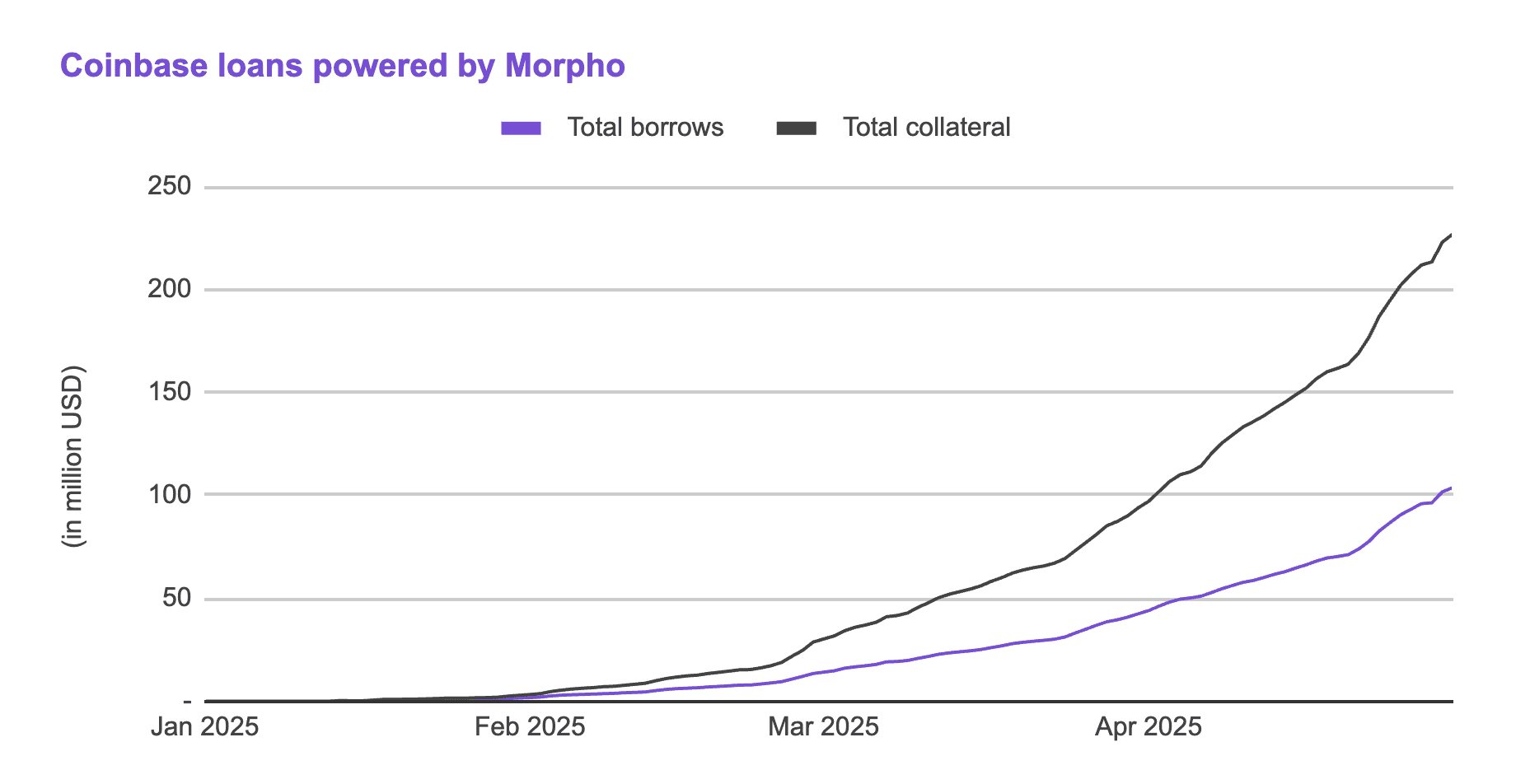

Traction-wise, several key indicators are at their highest levels to date. Stablecoin supply, a proxy for the activity on blockchains, saw three consecutive months of all time highs and reached $215bn by the end of the quarter. Coinbase announced a lending product built on Morpho’s decentralised infrastructure that allows retail users to access Bitcoin-backed loans through its frontend.

Until recently, DeFi and TradFi operated as two parallel financial systems that did not interact much with each other. It took many years for the underlying infrastructure to mature, DeFi protocols to be built, and for a supportive regulatory regime to emerge. We are now squarely in the middle of one of the most impactful shifts that will continue to play out over the coming years: the convergence of DeFi and TradFi.

Stablecoins & DeFi

In our view, two charts highlight the pivotal moment we are witnessing as DeFi and TradFi converge.

The first is the total supply of stablecoins.

Total stablecoin supply reached an all-time high of $215bn, reflecting growing blockchain adoption as stablecoins serve as the primary unit of account for many on-chain activities. What’s also interesting is that with over half of the supply being backed by U.S. Treasuries, stablecoins are emerging as a structural source of demand for both the U.S. dollar and short-term government debt.

Following our discussion last quarter of Bridge’s acquisition by Stripe, Stripe founders Patrick and John Collison used their annual letter to describe stablecoins as “room-temperature superconductors for financial services” and highlighted their native properties, speed, low cost, openness, and programmability, as improvements to the basic usability of money. Bridge’s existing customers already include SpaceX, which uses it to repatriate funds from Starlink sales abroad, and DolarApp, a neobank in Mexico that leverages Bridge to help individuals receive USD payments from various payroll providers. Past marking a significant validation point for stablecoins, Stripe continues to roll out tighter payment integrations and new product lines such as an incoming stablecoin-based card product.

The second chart is the total borrow of Coinbase loans powered by Morpho.

In January, Coinbase launched a Bitcoin-backed lending product powered by Morpho, allowing users to seamlessly take out USDC loans against their deposited BTC on Coinbase’s centralized platform. Behind the scenes, Coinbase moves the user’s BTC collateral on-chain, deposits it into Morpho smart contracts, and borrows USDC into the user’s Coinbase account. Initially released to a limited number of U.S. users, the product had already generated over $50m in borrow volume and $115m in deposited collateral by the end of Q1. The plan is to expand the product to more regions and broaden the collateral options to include additional crypto assets.

Regulation

One quarter in, it’s already clear that this administration is taking a radically different approach in working with the crypto industry compared to the previous one. The prior administration largely rejected productive dialogue with the industry and opted instead for a strategy of regulation by enforcement.

It’s hard to overstate the damage that was done. The SEC ended up targeting some of the industry’s leading companies that were forced to divert time and money to defend themselves, companies were discouraged from fully pursuing their product visions for fear of legal action, and perhaps most damaging of all, new entrepreneurs were scared away from entering the space.

The new administration has been very different. Following Gary Gensler’s resignation as SEC Chair, the new Chair established a Crypto Task Force focused on building a comprehensive framework for digital assets. Throughout Q1, the SEC also dropped several high-profile lawsuits initiated by the previous administration, including cases against Coinbase, Uniswap, Robinhood, OpenSea, and Kraken.

Finally, meaningful legislation is making its way through Congress across two separate topics: first, to provide overarching regulation and consumer protection over stablecoins, and second, a market structure bill that will clarify the respective roles of the SEC and CFTC over the issuance and trading of crypto assets.

Most notably, the GENIUS Act, which aims to regulate stablecoins, advanced significantly in Q1 2025. It passed the Senate Banking Committee with bipartisan support and is now heading to a full Senate vote. The bill includes strict reserve requirements, mandates transparency, and enforces AML/KYC standards for stablecoin issuers, while also tailoring oversight based on the size of the issuer.